Are You Fearful of Overpaying for a Home in an Unofficial Recession?

Many homebuyers find themselves sitting on the fence; paralyzed with the fear of overpaying for a home in a recession and then losing money on their investment with a possible market correct.

However, after taking a deeper look at the statistics, Tim and Emma are one of those couples that decided to continue with the purchase of a property despite the competitive nature of the local real estate market – but they almost didn’t take the leap out of fear vs education.

Like many would-be homeowners today, the fear of the unknown, the shortage of homes, as well as the tightening cost of living expenses made Tim and Emma pause and double-think about their goals to own a home.

What if they couldn’t find what they were looking for?

What if the cost of homes kept rising or the mortgage interest rates — or both?

What if they made a decision they couldn’t come back from?

They didn’t want to get stuck with something they would love and couldn’t afford.

Knowing whom to turn to is the first step in real estate success — in any market.

After sitting down with Lisa Ash and her valued mortgage consulting partners, Tim and Emma got a better outlook on their future as homeowners. They felt reassured that their dreams didn’t have to be packed away just because the path was a bit different than they originally thought it would be; or should be.

Once they understood the numbers, the history, and the trajectory of real estate in both of those aspects, there was renewed confidence that homeownership was not only going to achieve a sense of personal stability but could set them up for long-term financial success.

The key to their renewed confidence was education from industry experts that provided sound advice and solid information vs speculation and fear-driving headlines that caused the anxiety in the first place.

Yes. Housing prices are rising as are interest rates. But purchasing the right house at the right time under the right guidance and using the right resources (like a mortgage company that can readjust your mortgage rate on qualifying loans when rates come back down) can set a homebuyer on solid footing now.

Waiting just means more cost and time lost on investment growth.

Every situation is different, but we’re sharing some insights that could help make a difference for you.

Research Historical Market Trends Using Reputable Data & Expertise

One of the biggest steps Tim and Emma did before buying their new home was to consult with Lisa Ash to become educated about the market. Together, they researched and reviewed available data about the market to understand how it might affect their buying power, options, and strategies.

Although some of this information could be found on public resources and it would have been easy enough to turn to the media’s perspective of that data, Tim and Emma relied more on Lisa’s expertise to better understand local and national market patterns and current statistics.

As a professional REALTOR, Lisa has more complete and in-depth information available through professional resources like the MLS, as well as through professional data reporting tools available to REALTORS through the Minnesota Association of REALTORS, National Association of REALTORS, and the Saint Paul Area Association of REALTORS.

This provides a more complete and accurate insight into the current market conditions and outlook.

SO. What did Tim and Emma learn about the market that helped them move forward with a successful home purchase?

They learned history is not being repeated in this market. The housing crash in 2008 was actually the result of unchecked industry practices that started back in 1999 and resulted in a housing crisis that caused many homeowners to lose their homes or found themselves with negative equity.

That property loss was not simply the result of the excessive purchase prices that Tim and Emma had been hearing about and seeing in recent home sales activities. That market upset was due more in part because of the types of loans being used combined with the practice of excessive mortgage value extension – a common practice at the time that was unsustainable and doomed to fail all parties involved.

But that historical activity is not remotely the same situation for homeowners today.

Since that time in history, many preventative measures have been implemented in the appraisal and mortgage industries to protect homebuyers from potential harm. These measures have helped to further protect home buyers as well as home values.

They also learned why so many real estate and financial professionals continue to promote homeownership as a cornerstone for building wealth.

It’s easy to look at today’s headlines and think that home values and mortgage interest rates are out of control and locking would-be homebuyers out of the market, but a closer review of historical data and trends reveals a different narrative.

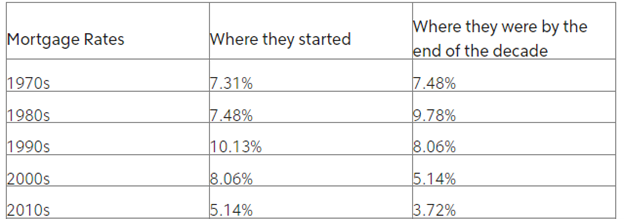

When we compare home value trends with mortgage rate trends it becomes clear that home buyers who wait to buy can lose valuable financial benefits in ownership.

While the 2% and 3% interest rates found between 2020 and 2021 created a uniquely favorable scenario for purchasing property, a 5% to 7% rate is more in line with U.S. historical averages.

And according to NAR Chief Economist, Lawrence Yun, MN real estate professionals, and local Minnesota homebuyers and sellers, shouldn’t expect to see interest rates as low as we saw in 2020-2021 again for at least the next 30-40 years.

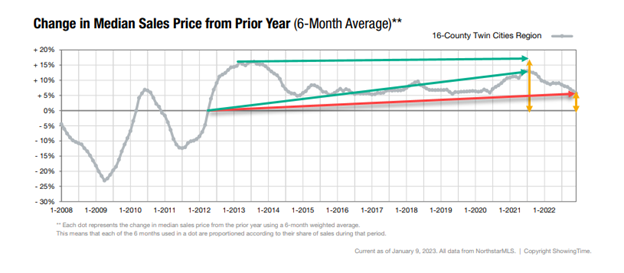

In comparison, home values have continued to climb at healthy rates while available inventory has steadily declined with growing populations over the years.

Like any investment, you’ll find times of growth and loss with real estate values, but as the data shows, equitable growth for homeowners across the 16-county metro area has always seen steady upward growth. Even the vast number of local pockets with large swings in appreciation between 2021 and 2022 were not as high as the jump in values following the market crash between 2007 and 2012.

A balanced market is one poised for long-term growth and strength; historically that market was found to be 4% to 5% appreciation as we’re beginning to see again in 2023.

When a homebuyer purchases a home with longevity as a part of their plans, they are certain to realize growth — similar to those who ‘play’ the stock market, but with better rates and more stability.

What about that monthly household budget?

Of course, we don’t dismiss the fact that a higher interest rate means a higher monthly mortgage payment, but it’s also dangerous for home buyers to dismiss the equitable growth potential when the right home is purchased at the right time. Homebuyers have the ability, with good credit history, to always refinance a mortgage to a lower interest rate when the opportunity presents itself, but buyers will never get back the time lost on the equitable rate of growth if they wait.

Historical data and trends are important but understanding the current market as they relate to location and timing is just as important.

Each community has its own trends and housing inventory statistics. Knowing where to look and when to make a move is something a full-time real estate professional can coach a homebuyer through.

With today’s continued shortage of properties, values in most locations are still strong and increasing even with a reduced number of closings and homes for sale. Yet, home buyers are still looking for some assurances that the home they purchase today won’t be upside down in months.

REALTORS like Lisa Ash have extensive knowledge, expertise, and experience in identifying properties in a variety of communities and neighborhoods that show potential vs those properties that could easily become money pits. Based on that knowledge and expertise, Lisa helps homebuyers like Tim and Emma to successfully negotiate a strong purchase agreement – one in their best interests and based on their short-term needs and long-term goals.

Understanding what is happening in the local market is the key to overcoming headlines that are designed to grab your attention and motivate readers out of fear. The fact is home values have steadily grown in the Twin Cities over the past decade.

This growth provides additional equity to current and would-be homeowners. Though values may not have increased as high in 2022 as they did in 2021, they are still increasing and helping owners build personal wealth.

Understanding Property Value Ebbs and Flows

As previously demonstrated, the real estate market has always recovered even when property values have fallen over several years as it did between 2007 and 2012. So even if equitable growth were to decelerate from the spectacular 13–33 percent value rises we observed across communities in the 16-county metro between 2021 and early 2022, the National Association of REALTORS believes the likelihood of most marketplaces experiencing a negative fall in a net valuation is slim due to the high housing demand.

And suppose it does occur, according to the estimates of professional economists, recovery time would only last for a short period; most likely in less than two years, and between a healthy 2% to 8 % growth depending on the market.

Tim and Emma realized that timing was a big key – a two-part timing key: when you purchase and how long you will live in or own your home.

Even at today's high-value purchase prices, a homebuyer is expected to see an improvement in their equitable position if they remain in their home for at least five years. Since the average number of years for homeownership rose to roughly 10.5 years in 2022, (according to First American Data & Analytics and Redfin), today’s homeowners are almost assured of realizing growth by the time they make another change to their mailing address.

That was welcomed news to Tim and Emma who are planning on raising a family in their new home.

Another Lesson Learned: Be Flexible

Who among renters doesn't have their sights set on a single-family home that has none of the walls shared with other tenants? But so do a lot of other people. That may mean the kind of property you desire will most likely come at a higher price than others in the market.

Many prospective buyers may be put off by monthly condo fees and shared walls, but purchasers of these kinds of homes frequently benefit from lower homeowner's insurance rates as well as other shared community amenities.

Townhome and condo Homeowner Association (HOA) fees generally cover much of the building and property maintenance and can include things community parks, picnic or pool areas, walking paths, and even community event rooms and more, making these types of options a great first step into homeownership.

Even while townhome and condominium appreciation typically increase at a slower rate than single-family homes, investing in one of these properties is a good opportunity, especially for first-time buyers, to get their feet wet financially and start accumulating equity.

Never forget that your first house is rarely the only one you will ever own. You can accumulate equity in a condo or townhome as well. This equity can eventually be used toward purchasing a single-family house in the future.

If you are planning to purchase a new home amidst a challenging market, your dreams may be fading due to the current economic climate. Is it truly the right time to get your first mortgage, considering that housing prices are continuing to rise and inflation is driving up the cost of basic living expenses? And if you wait, what is the possibility that you will be priced entirely out of the market?

Fear not; just like Tim and Emma, you must remember a few things before buying a house, even with inflation. First, keep in mind to always do your research and know your limits. Working with a Realtor who respects your limits is important as well.